BY NOAH YOSIF

Noah Yosif is an economist specializing in economic policy research pertaining to financial institutions and the federal banking system. He previously served in economic research roles at the U.S. Bureau of Labor Statistics, Department of the Treasury, and Federal Reserve Board. He is also a Master of Public Administration candidate at the Fels Institute of Government at the University of Pennsylvania, and holds a Masters in Applied Economics, as well as a Bachelors in Economics, from the George Washington University.

The coronavirus pandemic has engendered two threats to most countries’ socioeconomic wellbeing: sustained public health risks from a novel, deadly “superbug” as well as a severe economic fallout contingent upon the former’s containment. The recession induced by the coronavirus pandemic is unique in its ubiquity. While the consequences of previous global economic contractions have been limited to specific industries, countries, or both, the consequences of failed containment measures have enabled the coronavirus recession to afflict households, businesses, and sectors within advanced and developing economies alike. However, while its reach has been universally devastating, the virus’ ability to inflict long-term socioeconomic damage has varied due to remarkable inequalities between countries, which have enabled some to effectively mitigate the public health risks and economic fallout associated with the coronavirus pandemic much better than others.

According to the International Monetary Fund (IMF), countries spent a combined USD 13.1 trillion in various spending initiatives to mitigate the economic impact of the coronavirus pandemic. However, 78.8 percent of this spending was concentrated among just eleven advanced economies, all members of the Group of 20 (G20). This share goes up to 84.9 percent of all spending when a total of 27 advanced economies with similar financial capabilities is considered.[1] In other words, 153 emerging and low income-economies comprised just 15.1 percent of global spending targeted against the repercussions of the coronavirus pandemic. Yet, it is especially these countries many of which have limited fiscal resources at their disposal and may suffer from weak institutional capacity to absorb the economic consequences of a sustained global pandemic.[2] These inequalities have placed over 80 percent of the world population at risk of a protracted and inadequate economic recovery due to insufficient financial resources provided by their home countries.

It is important to explore the causes and consequences of inequalities between countries in their fiscal response to the coronavirus pandemic in order to better understand the trajectory of recovery facing the global economy at large. Such insights are essential to persuading policymakers within multilateral institutions and advanced economies of their essential role in ensuring that all economies have the necessary financial resources to shepherd their citizens through an extraordinary pandemic and recession.

Figure 1: Fiscal Spending by Economy Peer Group (Source: IMF Fiscal Monitor, World Bank, Author's Calculations)

Discrepancies in fiscal spending among advanced, emerging, and low-income economies can appear large if the size of the respective economy is not accounted for. However, data on pandemic-related spending compiled by the IMF suggest that emerging and low-income economies have devoted substantially fewer financial resources towards COVID relief as a share of gross domestic product (GDP) compared to advanced economies. Figure 1 compares average fiscal spending as a percentage of GDP as well as average fiscal spending per capita between five types of economies: advanced economies in the G20, other advanced economies, emerging economies in the G20, other emerging economies, and low-income economies. On average, fiscal spending among emerging and low-income economies comprised no more than 6 percent of total GDP, while advanced economies devoted between 10 and 20 percent of their GDP towards increased expenditures to mitigate the economic impact of the coronavirus pandemic.[3]

These discrepancies are even more pronounced when comparing fiscal expenditures per capita. Among low income economies, government spending as a percentage of GDP increased by over 70 percent in 2020. However, even this growth rate enabled the average citizen to only receive an estimated USD 34.44 to cope with the economic consequences of this historic global recession,[4] By contrast, government spending as a percentage of GDP among emerging economies rose by 44 percent. Here, however, this translated to between USD 437.63 and USD 497.58 in additional financial resources for the statistically average citizen.[5] Advanced economies, already reeling from a synchronized economic slowdown in 2019 as well as an uptick in government spending to mitigate heightened trade and geopolitical tensions,[6] managed to allocate between USD 5,100 and USD 8,700 per person throughout the coronavirus pandemic, over 255 times the average amount spent by a low-income country.[7]

Figure 2: Average Debt and estimated Debt Sustainability by Economy Peer Group (Source: World Bank)

Discrepancies in fiscal spending are not a product of choice or politics, but rather consequences of systemic inequalities in debt accumulation and financing. Figure 2 compares the average debt-to-GDP ratio and GNI for the same five country groups as of December 2019, just prior to the coronavirus pandemic. On average, emerging and low-income economies did not sport excessively high debt-to-GDP ratios compared to those of advanced and G20 emerging market economies. In fact, the average advanced economy retained a debt-to-GDP ratio three times that of most emerging and low-income economies. However, their capacity to carry additional debt, as denoted by GNI, was significantly more constrained compared to advanced economies and emerging economies in the G20. Using GNI as a metric of debt sustainability, a fairly complex calculation, some emerging and low-income economies retained nearly one-fiftieth the capital retained by an advanced economy.[8] Most fiscal spending measures were financed via debt, and those countries with greater debt sustainability had greater flexibility in terms of spending.[9]

Nearly half of all emerging markets and low-income economies were at an elevated risk of a debt crisis before the World Health Organization (WHO) declared the coronavirus a global pandemic in March of 2020.[10] The synchronized global slowdown in 2019 had already placed many of the affected countries in a uniquely precarious position compared to advanced economies, exacerbated by the flight of private capital into safe haven economies, limited access to hard currencies, declining commodity prices, decreased remittance inflows, and recessions or slow growth in global trade and tourism.[11] These factors, compounded by the inability of many emerging and low-income economies to access private capital markets or engage in deficit spending using their own currency, left many developing countries without the requisite capital reserves to finance essential fiscal spending programs at the same pace of advanced economies with greater debt sustainability.[12] Emerging and low-income economies often financed their debt via multilateral agencies or international capital markets which stipulate loan repayment in US dollars, thus increasing their exposure to interest rate risks.[13]

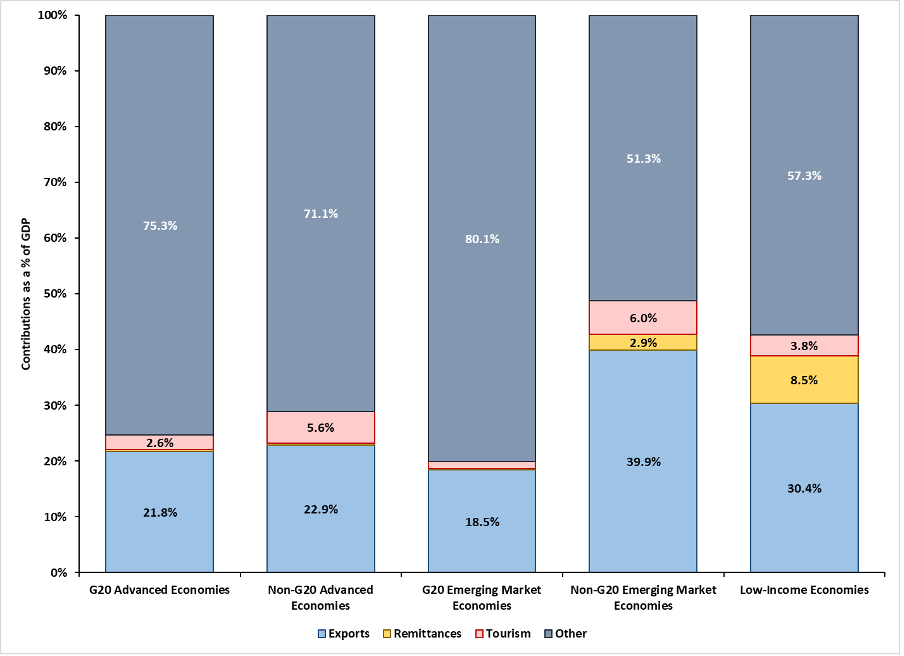

Figure 3: International Economic Dependence by Economy Peer Group (Source: World Bank, Author's Calculations)

In addition to difficulties securing debt financing from external sources, many emerging and low-income economies also struggled to raise capital internally from critical sectors such as commodities and international trade. Figure 3 depicts estimated contributions of exports, remittances, and tourism to the average GDP of each of the five country groups discussed above. On average, advanced and emerging economies in the G20 are not very dependent on international economic activity as such contributions encompass only about 25 percent of total GDP.[14] Economic activity in these countries is generally driven by domestic consumption and business investment, which are subject to their own downside risks, but much less dependent on the performance of the international economy at-large.[15] By contrast, other emerging and low-income economies, are quite dependent on international economic activity, with these contributions comprising between 44 and 48 percent of total GDP on average.[16] These numbers highlight major vulnerabilities among many developing countries to short-term shocks in international economic activity.

Unfortunately, tourism, travel, and trade will likely require a protracted timeframe of recovery to reach pre-coronavirus pandemic levels. Recent forecasts from the IMF and World Bank note that while supply chain adjustments and technological advancements have enabled global commerce to rebound more quickly than expected, normalization of cross-border travel faces a lengthy return to pre-pandemic levels.[17] Given the possibility of a prolonged recovery for critical economic sectors in conjunction with limited external debt financing opportunities, many emerging and low-income economies will be unable to offset the economic consequences of the coronavirus pandemic via fiscal spending without risking an unsustainable accumulation of debt. This could perpetuate a vicious cycle which would leave emerging and low-income economies unable to mount an effective economic recovery, exacerbating global poverty and inequality.

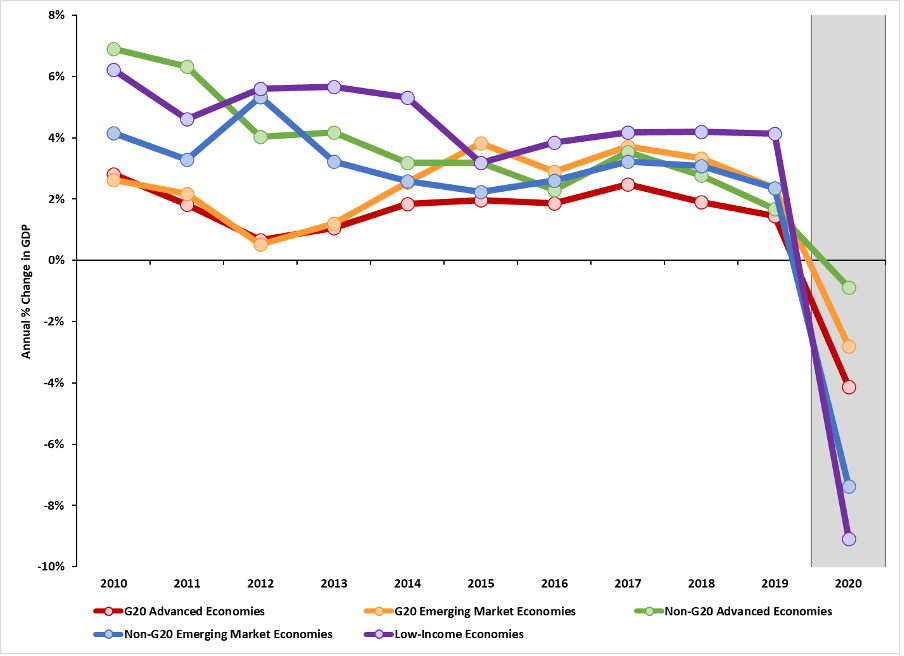

Figure 4: Annual Change in GDP by Economy Peer Group (Source: World Bank, Trading Economics, Author's Calculations)

The implications from these discrepancies in fiscal spending are already evident, placing countries at staggered starting points from which to commence their recoveries. Figure 4 shows the average annual percent change in real GDP for each of the five groups of economies discussed here. Prior to the coronavirus pandemic, nearly all economies experienced increased macroeconomic headwinds due to the synchronized global slowdown in 2019. However, during the onset of the coronavirus pandemic in 2020, economies experienced varying rates of contraction, which were influenced to a significant degree by the extent of fiscal measures enacted to soften the shock of a slowdown in consumer and business activity due to containment measures preventing the spread of coronavirus.[18] While advanced economies and G20 emerging economies exhibited declines between 0.1 and 0.4 percent, non-G20 emerging and low-income economies were set back further, showing declines between 0.7 and 0.9 percent.[19]

These staggered declines in growth and recovery are a stark reminder of the coronavirus pandemic’s exacerbation of global inequalities between countries. According to recent research by the IMF, many low-income economies would require an additional USD 200 billion between 2021 and 2025 to maintain an adequate cadence of recovery and supplement existing financial buffers to prevent potential aftershocks.[20] Such downside scenarios, including concentrated contractions in developing countries as well as a slower global recovery, would require an additional USD 100 billion in financing to these economies.[21] However, this timeframe may still be insufficient to prevent major economic scarring via poverty and inequality. According to the United Nations, over 32 million people in 47 of the world’s least developed countries could face extreme poverty due to increased inequalities in healthcare, education, and employment opportunities until 2025.[22]

It is imperative for policymakers within multilateral institutions and advanced economies to ensure that all economies, regardless of income, have the ability to enact adequate fiscal spending measures that mitigate the impact of the coronavirus pandemic on their citizens. Such initiatives will require cooperation between multilateral agencies and private sector donors to ensure sufficient capital reserves are available for all at-risk emerging and low-income economies.[23] Creditors will also need to provide reasonable debt relief or restructuring options that account for countries’ debt sustainability, vulnerability to additional shocks, and likelihood of a protracted economic recovery. In the event that demand for capital by emerging and low-income economies outpaces supply, policymakers may need to consider more unorthodox measures such as expanded allocation of the IMF’s global reserve currency, known as Special Drawing Rights,[24] or a freeze in sovereign credit downgrades which make borrowing costs prohibitively expensive while serving as a red-flag for potential investors.[25] Multilateral agencies have already begun addressing some of these issues: As of February 2021, the World Bank had issued USD 14.2 million in loans to low-income countries and another USD 37 million in loans to lower-middle-income countries.[26] Yet, as Justin Sandefur notes, low-income countries saw GDP growth decline by over 6 percentage points, while these commitments and actual disbursals account for just 1.7 percent of lost growth.[27] Furthermore, the IMF has prepared $21 billion in Special Drawing Rights for low-income countries as reserves[28]; yet, this is subject to agreement by its collective membership on the procedures for each borrowing nation to exchange their share for other currencies and how wealthier nations may redistribute their own Special Drawing Rights allocations to low-income countries[29]. These bureaucratic obstacles could confound the timely distribution of essential aid to low-income countries which are continuing to suffer from an ongoing pandemic and concurrent economic crisis.

Figure 5: Vaccinations by Month and Economy Peer Group (Source: Our World in Data/Oxford University, Author's Calculations)

Yet, the most important determinant of countries’ economic recovery will be containment of the coronavirus pandemic itself. Figure 5 shows vaccination rates as a percentage of the total population per month among all five economies discussed above. Today, over 10 percent of the total population within the G20 advanced economies are vaccinated, while most emerging and low-income economies have vaccinated less than 5 percent of their total populations, on average.[30] According to some studies, over 90 percent of the population in these countries will not see a single vaccine shot administered in 2021.[31] The recession induced by the coronavirus pandemic is an exogenous shock, which means that vaccinations will be essential to enabling these countries to reopen their economies and recover in tandem with the global economy. Efforts to ensure emerging and low-income nations have access to vaccines, such as the Covax Program administered by WHO, will be just as critical to their economic wellbeing as those aimed at supporting their fiscal spending abilities.[32] However, Covax is a prime example of how such efforts are already facing a multitude of challenges, including severe underfunding, delays in distribution, as well as vaccine hoarding, all of which have limited available supply.[33] Furthermore, many of the advanced economies that host vaccine manufacturers, including Moderna, Pfizer, and Johnson & Johnson, have resisted demands for patent restrictions and waving intellectual property rights. These measures, if they are not thwarted by governments in the Global North, could enable low-income countries to ramp up their own vaccine production and distribution networks.[34]

Most economists, academics, and policymakers agree that the costs of fiscal action to mitigate the impact of the coronavirus pandemic are significantly lower than the costs of inaction. Yet, most emerging and low-income economies have been forced down the path of relative inaction given systemic inequalities in debt financing in conjunction with reduced prospects for recovery in the short-term. Their shortcomings not only threaten the socioeconomic wellbeing of over 3.6 billion individuals, but risks a fragmented recovery excluding millions of households, businesses, and industries within the international economy. As vaccines continue to bring a post-coronavirus reality closer, policymakers within multilateral institutions and advanced economies must ensure all countries can enact reasonable fiscal measures that enable their economies to weather this crisis, including cooperation between multilateral agencies and private sector donors, reasonable debt relief and restructuring options, as well as increased access to vaccines, the real keys to economic recovery from a global pandemic. If these inequalities are allowed to fester, the continuation of new coronavirus outbreaks, and their equally devastating economic consequences could further stall the global recovery, or create significant scars which will be difficult to reverse in the long-term[35]. By ensuring economies of all statures have the opportunity to enact adequate fiscal spending measures on behalf of their constituents, we will be one step closer to a prognosis for prosperity that is within reach for all.

REFERENCES

[1] International Monetary Fund Fiscal Affairs Department. “IMF Fiscal Monitor – October 2020,” October 14, 2020.

[2] Ibid.

[3] Ibid.

[4] Ibid.

[5] Ibid.

[6] Gopinath, Gita. “The World Economy: Synchronized Slowdown, Precarious Outlook.” IMFBlog (blog). International Monetary Fund, October 15, 2019. https://blogs.imf.org/2019/10/15/the-world-economy-synchronized-slowdown-precarious-outlook/.

[7] International Monetary Fund Fiscal Affairs Department. “IMF Fiscal Monitor - October 2020,” October 14, 2020.

[8] World Bank Office of the Chief Economist. “World Bank Databank,” December 2020.

[9] Ibid.

[10] Weaver, Catherine, and Rachel Rosenberg. “The New Debt Trap: COVID-19 and Global Development.” News. LBJ School of Public Affairs, December 8, 2020. https://lbj.utexas.edu/resiliency-toolkit/debt#_edn17.

[11] Arezki, Rabah, and Shanta Devarajan. “Fiscal Policy for COVID-19 and Beyond.” Future Development (blog). The Brookings Institution, May 29, 2020. https://www.brookings.edu/blog/future-development/2020/05/29/fiscal-policy-for-covid-19-and-beyond/.

[12] Vijaya, Ramya. “How the Pandemic Is Hurting Developing Countries’ Economies.” Pandemic Exposes Financial Inequities. U.S. News & World Report, December 15, 2020. https://www.usnews.com/news/best-countries/articles/2020-12-15/covid-19-exposes-inequalities-in-the-global-financial-system.

[13] Ibid.

[14] International Monetary Fund Fiscal Affairs Department. “IMF Fiscal Monitor - October 2020,” October 14, 2020.

[15] Kharroubi, Enisse, and Emanuel Kohlscheen. "Consumption-led expansions." BIS Quarterly Review, March (2017).

[16] International Monetary Fund Fiscal Affairs Department. “IMF Fiscal Monitor - October 2020,” October 14, 2020.

[17] Martin, Eric. “IMF Lifts Global Growth Forecast, Warns of Diverging Rebound.” Economics. Bloomberg, April 6, 2021. https://www.bloomberg.com/news/articles/2021-04-06/imf-boosts-global-growth-forecast-warns-of-diverging-rebound.

[18] Benmelech, Efraim, and Nitzan Tzur-Ilan. The Determinants of Fiscal and Monetary Policies during the COVID-19 Crisis. No. w27461. National Bureau of Economic Research, 2020.

[19] International Monetary Fund Fiscal Affairs Department. “IMF Fiscal Monitor - October 2020,” October 14, 2020.

[20] Gregory, Robert, Gaëlle Pierre, Luiza Antoun de Almeida, Heiko Hesse, Anne-Charlotte Paret, and Ke Wang. Tech. Macroeconomic Developments and Prospects in Low Income Countries —2021. International Monetary Fund, March 30, 2021. https://www.imf.org/en/Publications/Policy-Papers/Issues/2021/03/30/Macroeconomic-Developments-and-Prospects-In-Low-Income-Countries-2021-50312.

[21] Ibid.

[22] Traeger, Rolf, Benjamin Mattondo Banda, Matfobhi Riba, Giovanni Valensisi, Kyeonghun Joo, Tobias Lechner, Anja Slany, et al. Rep. The Least Developed Countries Report 2020. United Nations, December 3, 2020. https://unctad.org/system/files/official-document/ldcr2020_en.pdf.

[23] Weaver, Catherine, and Rachel Rosenberg. “The New Debt Trap: COVID-19 and Global Development.” News. LBJ School of Public Affairs, December 8, 2020. https://lbj.utexas.edu/resiliency-toolkit/debt#_edn17.

[24] Gallagher, Kevin, José Antonio Ocampo, and Ulrich Volz. "Special Drawing Rights: International Monetary Support for Developing Countries in Times of the COVID-19 Crisis." The Economists’ Voice 1, no. ahead-of-print (2020).

[25] Mutize, Misheck. “Africa's Post-Covid Debt Crisis Is Being Aggravated by Unreliable Data, Ratings Agencies.” Quartz Africa. Quartz, October 23, 2020. https://qz.com/africa/1921741/africa-covid-debt-crisis-worsened-by-poor-data-moodys-fitch-sp/.

[26] Sandefur, Justin, and Julian Duggan. “Tracking the World Bank's Response to COVID-19.” Commentary & Analysis. Center For Global Development, April 5, 2021. https://www.cgdev.org/blog/tracking-world-banks-response-covid-19.

[27] Ibid.

[28] Andersson, Magdalena, Kristalina Georgieva, and Gerry Rice. In IMFC Press Briefing, 2021. https://www.imf.org/en/News/Articles/2021/04/08/tr040821-transcript-of-the-imfc-press-briefing.

[29] Mark, Jeremy, and Vasuki Shastry. “A World Apart: How Wealthy Nations Can Strengthen the COVID Safety Net.” New Atlanticist. Atlantic Council, April 21, 2021. https://www.atlanticcouncil.org/blogs/new-atlanticist/a-world-apart-how-wealthy-nations-can-strengthen-the-covid-safety-net/.

[30] Roser, Max, Hannah Ritchie, Esteban Ortiz-Ospina, and Joe Hasell. “Coronavirus Pandemic (COVID-19).” Oxford University: Oxford University, April 6, 2021.

[31] “9 Out of 10 People in Poor Countries Set to Miss Out on COVID-19 Vaccine Next Year.” News. Amnesty International, December 9, 2020. https://www.amnesty.org/en/latest/news/2020/12/campaigners-warn-that-9-out-of-10-people-in-poor-countries-are-set-to-miss-out-on-covid-19-vaccine-next-year/.

[32] Sachs, Jeffrey D., Salim Abdool Karim, Lara Aknin, Joseph Allen, Kirsten Brosbøl, Gabriela Cuevas Barron, Peter Daszak et al. "Priorities for the COVID-19 pandemic at the start of 2021: statement of the Lancet COVID-19 Commission." The Lancet (2021).

[33] Ravelo, Jenny Lei. “With Scarce Funding for ACT-A, 'Everything Moves Slower': WHO's Bruce Aylward.” Devex. Devex, February 22, 2021. https://www.devex.com/news/with-scarce-funding-for-act-a-everything-moves-slower-who-s-bruce-aylward-99195.

[34] Ravelo, Jenny Lei. “Is Covax Part of the Problem or the Solution?,” March 11, 2021. https://www.devex.com/news/is-covax-part-of-the-problem-or-the-solution-99334.

[35] The Associated Press. “Worldwide Covid-19 Death Toll Tops 3 Million as CRISIS DEEPENS Brazil, India and France,” April 17, 2021. https://www.nbcnews.com/health/health-news/worldwide-covid-19-death-toll-tops-3-million-crisis-deepens-n1264378.

PHOTO CREDIT: Free use image from Canva Pro.